Welcome to the L.E.K. Consulting Consumer Cost-Of-Living Tracker – our unique lens on consumer attitudes to the challenges they face.

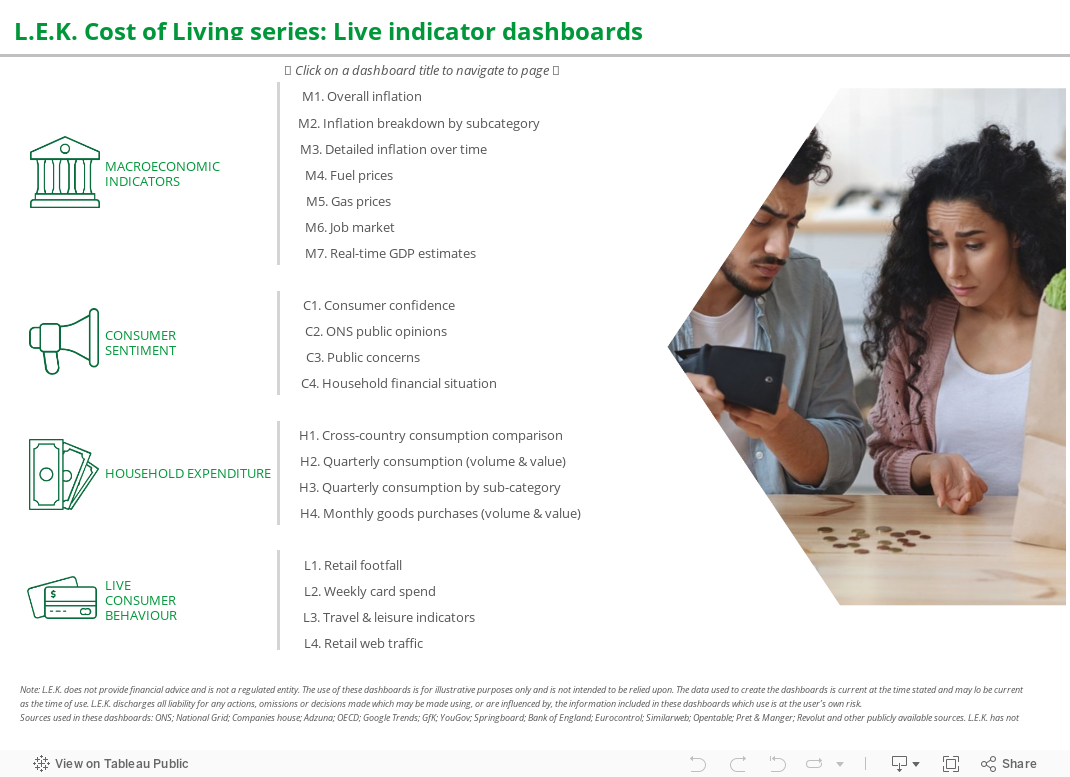

Macroeconomic

environment

The dynamics shaping the costs of goods and services and consumers' ability to pay them.

Household

expenditure

A high-level look at where consumers are prioritising their spending.

Consumer

behaviour

The trends and behaviours that are shaping consumer spending habits.

By leveraging data from respected sources including YouGov, we have created our own bespoke view of the ever-changing effects of the economic and social climates on consumer spending habits. Updated regularly, by aggregating data from a wide range of sources and filtering it through our unique experience and perspective, the L.E.K. Cost-Of-Living-Tracker is an essential tool for any business looking to understand the impact of evolving consumer behaviours. As cost of living pressures play out, we look forward to providing the insights consumer-facing businesses need to develop a winning strategy.

How to Use the Cost-of-Living Dashboard

Watch our one-minute explainer video to see how to get the most out of the Cost-of-Living Tracker.

Monthly update

March 2024

December and January provided cause for hope in terms of consumer spending. We saw a shift towards cautious optimism, due to discussions of potential interest rate cuts as early as April (though rates now confirmed to be held at the current rate for at least another month). There was also moderate uplift in consumer sentiment, with overall consumer confidence read at (-)19 in January, the highest level since February 2022.

February has been mixed in terms of macroeconomic developments. Real wages have continued to grow, and business activity expansion outperformed most estimates despite supply chain challenges. However, retail sales saw weaker performance, growing by only 1.9%, the slowest growth since September 2022; consumer confidence also deteriorated slightly.

Despite this, cautious optimism remains the prevailing theme, with only a limited indication of movement in either direction away from this. A more substantial shift in mood is likely to require a definite trigger, like an interest rate reduction or a reduction in the prevailing inflation rate.

Despite the backdrop portrayed above, we saw the positive trend in consumer sentiment towards travel and leisure continue. Discretionary spend has been strikingly resilient in light of cost-of-living pressures, in defiance of early indications from consumers that they might need to cut back in this area. This is reinforced by findings from our recent proprietary travel and leisure survey of 1,300-plus consumers in the UK, where 80%-90% of consumers across most consumer segments, age groups and income bands indicated that their discretionary spend in 2024 would not decline vs 2023. Interestingly, within the discretionary spend basket, travel spend continues to command a primary position. Approximately 90% of respondents expected to spend more on holidays in 2024 than they did in 2023, with continued post-COVID-19 interest in international travel, especially among younger age groups. The survey also showed, however, that takeaway food, eating out and alcoholic drinks are more likely to experience a contraction in spend if cost pressures persist.

This is a good sign for travel businesses, as airline and other transport capacity continues to recover, and grow in the case of ocean and river cruises. There is likely to be renewed interest seen in specialist categories (e.g. cruising) and experiential travel on the back of growing interest among middle to higher-income groups. Although at this stage it is premature to draw definitive conclusions based on expressed interest by consumers, these are encouraging signs for the travel sector ahead of the peak summer holiday period and at the time when operators start to shape their inventories and holiday programmes for 2025.

“The travel sector continues to stand out within the consumer landscape, with consistent positive intent amongst a broad base of consumers. We think this is creating opportunities across the board — from tour operators catering to more affluent holidaymakers looking for luxury overseas trips to brands targeting new-age travellers seeking something immersive/experiential to agents (or park-based operators) focused on families that want an enjoyable time spent together that is a good value for the money. The key for operators remains having a clear understanding of their target consumer(s) and their evolving behaviours and a compelling contemporary proposition that aligns well to those preferences priorities.”

Mark Boyd-Boland, Consumer Partner

Keep informed of updates to the tracker and ever-evolving consumer spending habits.

Sign-up for updatesBoth now and as consumer confidence recovers, up-to-date information about household spending and sentiment is vital for any consumer-facing business. The L.E.K. Cost-of-Living Tracker delivers the real-time view that is so essential to developing the right commercial strategy.

Dominic Miles, L.E.K. Partner and Global Co-Head of L.E.K.’s Consumer Sector

Connect with Dominic.

Connect with L.E.K.

The Tracker provides critical insights for brands, retailers and investors in consumer-facing businesses as they think about their growth strategy, performance improvement and M&A – and we hope reveals increasing confidence in consumer sectors as 2023 unfolds.

Mark Boyd-Boland, L.E.K. Partner

Connect with Mark.

Connect with L.E.K.

The L.E.K. Consumer

Cost-of-Living Tracker

To understand what this data means for your business, get in touch with your questions by filling in the form below.